Consolidation Strategy Aims to Lift Long-Term Profitability

The Adani Group’s cement business is entering a new phase of structural integration, a move that investors have been expecting ever since the group acquired Ambuja Cements and ACC from Holcim India nearly three years ago. In a sector where cement remains a price-sensitive, commodity-driven product, scale and cost efficiency are often the strongest levers of sustainable profitability. The proposed amalgamation seeks to pull all these levers at once.

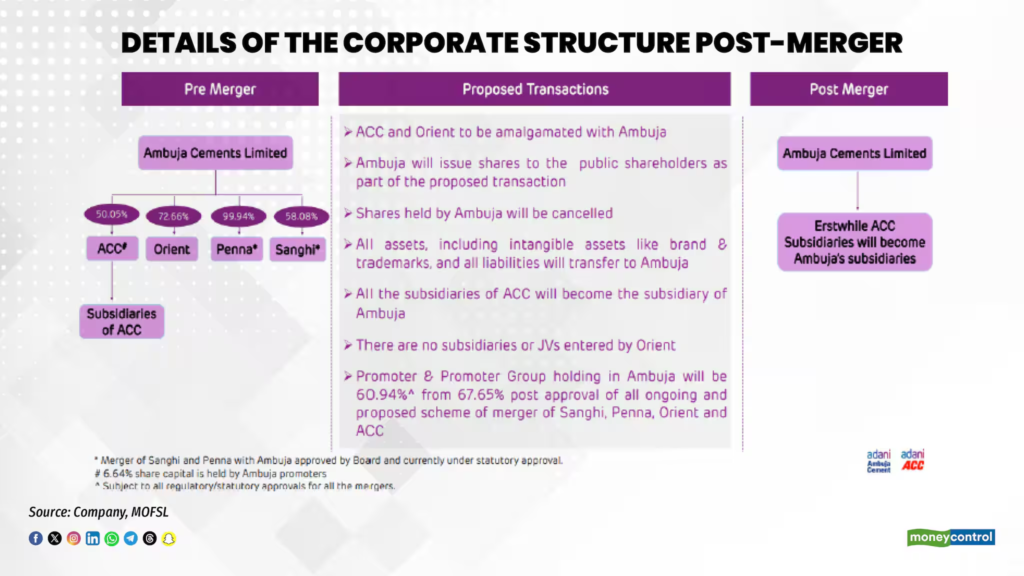

Under the announced plan, multiple cement entities within the group—including ACC and its subsidiaries, Orient Cement, Penna Cement, and Sanghi Industries—will be brought under Ambuja Cements. The transaction involves no cash outflow; instead, it will be executed through a share-swap arrangement. Based on market feedback, the swap ratios appear broadly reasonable, though the promoter group’s stake in Ambuja may reduce to about 60.9 percent from the current 67.5 percent after completion.

Creating a Unified Cement Platform

Once completed, the consolidation will create a pan-India cement major with an installed capacity of roughly 107 million tonnes per annum. The combined network will include 24 integrated cement plants, 22 grinding units, and more than 116 ready-mix concrete facilities, all operating under a simplified corporate structure.

According to management, this integration is expected to streamline operations across manufacturing, logistics, branding, and sales. Importantly, it will also eliminate overlapping master supply agreements and related-party transactions, improving transparency and governance.

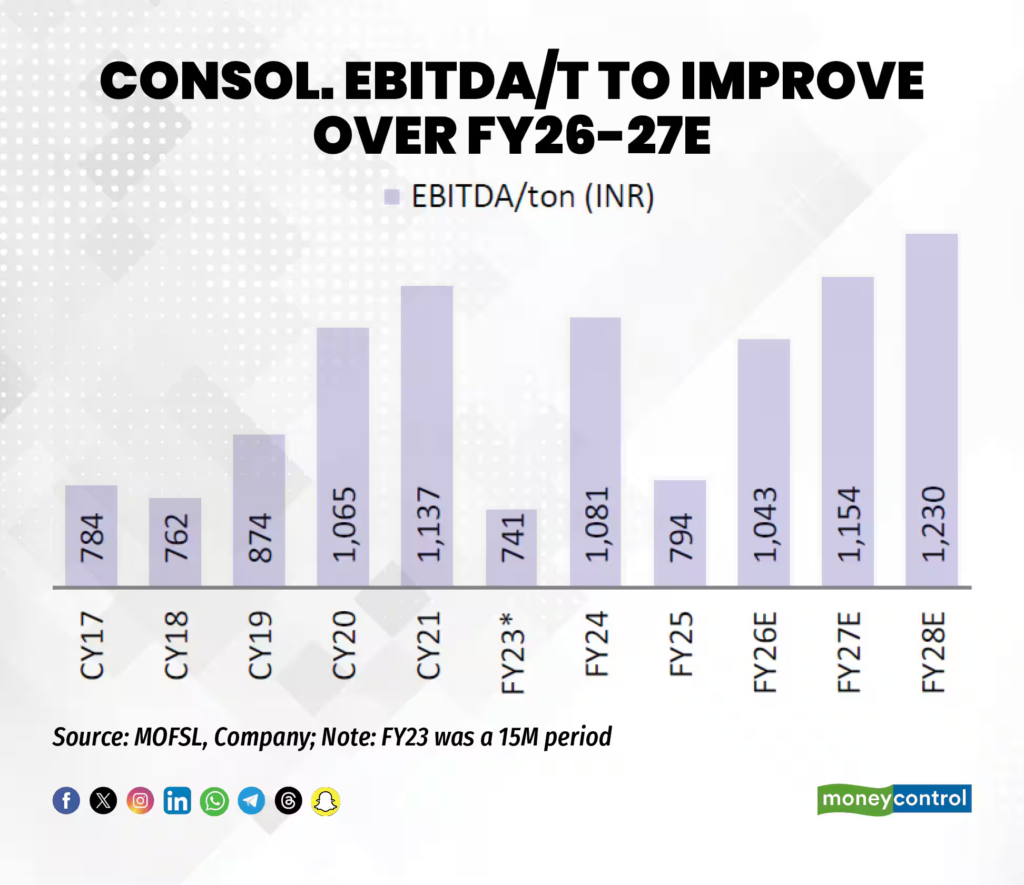

One of the most significant takeaways from the announcement is the projected cost synergy of approximately ₹100 per tonne. In an industry where incremental savings directly impact margins, this is a material improvement.

Cost Reduction and Margin Expansion

Management has earlier outlined a clear roadmap for cost optimisation. Manufacturing costs, currently estimated at around ₹4,200 per tonne, are targeted to decline to ₹4,000 per tonne by FY26 and further to ₹3,650 per tonne by FY28. If executed successfully, this would place Ambuja among the lowest-cost producers in the domestic cement industry.

Ambuja already stands out in terms of profitability. Despite monsoon-related demand softness across the sector in the September quarter, the company reported an EBITDA per tonne of ₹1,061, comfortably above the industry average and higher than the year-ago period, according to brokerage estimates.

Strong Geographic Presence and Brand Continuity

Another advantage lies in Ambuja’s balanced regional footprint. The merged entity will have meaningful exposure across all major demand zones in India, with a stronger presence expected in high-growth regions such as North and Central India by the end of FY26.

Crucially, the merger does not dilute brand equity. Both Ambuja and ACC brands will continue independently, leveraging their distinct positioning and customer loyalty.

Digital Push and Competitive Context

The timing of the consolidation also aligns with the group’s broader digital transformation efforts. Analysts note the adoption of an “Integrated Intelligence” framework that applies digital tools across quarrying, production, and logistics—an initiative aimed at improving efficiency and decision-making.

From a competitive standpoint, the move helps the Adani Group keep pace with UltraTech Cement, India’s largest cement producer, which is also expanding capacity steadily. In cement, scale often translates into pricing discipline, stronger realisations, and better margins.

Consensus estimates suggest that the combined benefits of scale, consolidation, and cost control could lift EBITDA margins by 200–300 basis points by FY27.

Risks to Monitor

That said, the cement industry remains cyclical. Periods of excess capacity coupled with weak demand can pressure prices, cash flows, and returns. Additionally, valuations in the sector are already on the higher side, which may explain the market’s muted initial reaction to the announcement.

Overall, the proposed amalgamation positions Ambuja Cements for stronger operational efficiency and long-term value creation, provided execution stays on track and demand conditions remain supportive.